---

date: 2024-11-09

title: "Bayesian Inference in the NDLM: Part 2"

subtitle: Time Series Analysis

description: "Normal Dynamic Linear Models (NDLMs) are a class of models used for time series analysis that allow for flexible modeling of temporal dependencies."

categories:

- Bayesian Statistics

- Time Series

keywords:

- Time series

- Filtering

- Smoothing

- NDLM

- Normal Dynamic Linear Models

- Seasonal NDLM

- Superposition Principle

- R code

fig-caption: Notes about ... Bayesian Statistics

title-block-banner: images/banner_deep.jpg

---

## Filtering, Smoothing and Forecasting: Unknown observational variance :movie_camera: {#section-NDLM-unknown-variance}

::: {.callout-tip collapse="false"}

## Recap:

In [@sec-Bayesian-inference-NDLM-known-variances] we performed Bayesian inference on [@eq-inference-NDLM], an NDLM with known observational variance $\nu_t$ and system variance $\boldsymbol{\omega}_t$ c.f.and determined that under the assumption of a normal prior $(\theta_0 \mid \mathcal{D}_0) \sim \mathcal{N}(\mathbf{m}_{0}, \mathbf{C}_{0})$, with

filtering leads to a posterior $p(\boldsymbol{\theta}_t|\mathcal{D}_t) \sim N (\mathbf{m}_t, \mathbf{C}_t)$

and smoothing leads to normal posterior distributions

In this lesson we will explore the case of the NDLM, where we **assume** That the observational variance $\nu_t=v$ i.e. is constant over time.

:::

### Inference in the NDLM with unknown constant observational variance:

Let $\nu_t = v\ \forall t$ with $\nu$ unknown and consider a DLM with the following structure:

$$

\begin{aligned}

y_t &= \mathbf{F}_t^\top \boldsymbol{\theta}_t + \nu_t,

&\nu_t &\sim \mathcal{N} (0, \nu)

&\text{(obs)}\\

\boldsymbol{\theta}_t &= \mathbf{G}_t \boldsymbol{\theta}_{t-1} + \boldsymbol{\omega}_t,

& \boldsymbol{\omega}_t

&\sim \mathcal{N} (0, \nu \mathbf{W}^*_t)

&\text{(sys)}

\end{aligned}

$$ {#eq-NDLM-unknown-variance}

- where we have the usual suspects:

- An observation equation, relating the observed $y_t$ to the hidden state $\theta_t$ plus some sensor noise $\nu_t$.

- A state equation, which describes how the hidden state $\theta_t$ evolves plus some process noise $\boldsymbol{\omega}_t$,

- $\mathbf{F}_t$ is a *known* observation operator,

- $\mathbf{G}_t$ is a *known* state transition operator,

- $\boldsymbol{\theta}_t$ is the hidden state vector, and

- $\boldsymbol{\omega}_t$ is the process noise, e.g. friction or wind.

- $\mathbf{W}_t$ is a *known* covariance matrix, for process noise.

::: {.callout-important collapse="False"}

## Question: why does $\nu$ appear in the $w_t$ distribution equation? {.unnumbered}

Prado says is also **assuming** that the system noise is conditional on the variance $\nu$.

Yet this seems to be an assumption that should be justified.

In fact, What we are missing is a logical Model for this model i.e. simple use case

:::

with conjugate prior distributions:

$$

\begin{aligned}

(\boldsymbol{\theta}_0 \mid \mathcal{D}_0, \nu) &\sim \mathcal{N} (\mathbf{m}_0, \nu\ \mathbf{C}^*_0) \\ (\nu \mid \mathcal{D}_0) &\sim \mathcal{IG}\left(\frac{n_0}{2}, \frac{d_0}{2}\right ) \\

d_0 &= n_0 s_0

\end{aligned}

$$ {#eq-NDLM-unknown-variance-priors}

### Filtering

We now consider filtering updating uncertainty. Which lets us infer current time step parameters or observation based on the previous time step's information and $\nu$ as being normal distributed.

we will be interesting the following distributions:

- $p(\boldsymbol{\theta}_t \mid \mathcal{D}_{t−1})$ the prior density for the state vector at time t given information up to the preceding time;

- $p(y_t \mid \mathcal{D}_{t−1})$ the one-step-ahead predictive density for the next observation;

- $p(\boldsymbol{\theta}_t \mid \mathcal{D}_t)$ the posterior density for the state vector at time t given $\mathcal{D}_{t−1}$ and $y_t$;

- the h-step-ahead forecasts $p(y_{t+h} \mid \mathcal{D}_t)$ and $p(\boldsymbol{\theta}_{t+h} \mid \mathcal{D}_t)$;

- $p(\boldsymbol{\theta}_t \mid \mathcal{D}_T)$ the smoothing density for $\boldsymbol{\theta}_t$ where $T > t$.

Assuming:

$$

(\boldsymbol{\theta}_{t-1} \mid \mathcal{D}_{t-1}, \nu) \sim \mathcal{N} (\mathbf{m}_{t-1}, \nu\ \mathbf{C}^*_{t-1})

$$

By filtering we obtain the next time step parameters conditional on the previous time step's information and the variance $\nu$ as being normal distributed.

$$

\begin{aligned}

(\boldsymbol{\theta}_t \mid \mathcal{D}_{t-1}, \nu) &\sim \mathcal{N} (\mathbf{a}_t, \nu \mathbf{R}^*_t) \\

\mathbf{a}_t &= \mathbf{G}_t \mathbf{m}_{t-1} \\

\mathbf{R}^*_t &= \mathbf{G}_t \mathbf{C}^*_{t-1} \mathbf{G}'_t + \mathbf{W}^*_t

\end{aligned}

$$ {#eq-NDLM-unknown-variance-filtering}

We can also marginalize $\nu$ by integrating it out, we have parameters that are unconditional on $\nu$:

$$

\begin{aligned}

(\boldsymbol{\theta}_t \mid \mathcal{D}_{t-1}) &\sim T_{n_{t-1}} (\mathbf{a}_t, \mathbf{R}_t) \\

\mathbf{R}_t &\equiv s_{t-1} \mathbf{R}^*_t

\end{aligned}

$$ {#eq-NDLM-unknown-variance-filtering-unconditional}

with $s_t\ \forall t$ given in @eq-NDLM-unknown-variance-filtering.

- $(y_t \mid \mathcal{D}_{t-1}, \nu) \sim \mathcal{N} (f_t, \nu q^*_t)$

- with

- $f_t = F'_t \mathbf{a}_t$

- $q^*_t = (1 + F'_t \mathbf{R}^*_t F_t)$

and unconditional on $\nu$ we have

- $(y_t \mid \mathcal{D}_{t-1}) \sim T_{n_{t-1}} (f_t, q_t)$

- with

- $q_t = s_{t-1} q^*_t$

- $(v \mid \mathcal{D}_t) \sim \mathcal{IG}\left( \tfrac{n_t}{2}, \tfrac{s_t}{2}\right )$

- with

- $n_t = n_{t-1} + 1$

$$

s_t = s_{t-1} + \frac{s_{t-1}}{n_t} \left ( \frac{e^2_t}{q^*_t} - 1 \right ),

$$ {#eq-NDLM-unknown-variance-filtering}

here $e_t = y_t - f_t$

- $(\theta_t \mid D_t, v) \sim N (m_t, vC^*_t)$,

- with

- $m_t = a_t + A_t e_t$, and

- $C^*_t = R^*_t - A_t A'_t q^*_t$.

Similarly, unconditional on $\nu$ we have

- $(\boldsymbol{\theta}_t\mid \mathcal{D}_t) \sim T_{n_t} (\mathbf{m}_t, \mathbf{C}_t)$

- with

- $\mathbf{C}_t = s_t \mathbf{C}^*_t$

### Forecasting

Similarly, we have the forecasting distributions:

- $(\boldsymbol{\theta}_{t+h} \mid \mathcal{D}_t) \sim T_{n_t} (\mathbf{a}_{t}(h), \mathbf{R}_{t}(h))$,

- $(y_{t+h} \mid \mathcal{D}_t) \sim T_{n_t} (f_{t}(h), q_{t}(h))$,

- with

- $\mathbf{a}_{t}(h) = \mathbf{G}_{t+h} \mathbf{a}_{t}(h-1)$,

- $\mathbf{a}_{t}(0) = \mathbf{m}_t$, and

$$

\begin{aligned}

\mathbf{R}_{t}(h) &= \mathbf{G}_{t+h} \mathbf{R}_{t}(h-1) \mathbf{G}'_{t+h} + \mathbf{W}_{t+h} \\

\mathbf{R}_{t}(0) &= \mathbf{C}_t

\end{aligned}

$$

$$

f_{t}(h) = \mathbf{F}'_{t+h} \mathbf{a}_{t}(h) \qquad q_{t}(h) = \mathbf{F}'_{t+h} \mathbf{R}_{t}(h) \mathbf{F}_{t+h} + s_{t}

$$

### Smoothing

Finally, the smoothing distributions have the form:

$$

(\boldsymbol{\theta}_t \mid \mathcal{D}_T) \sim T_{n_T} (a_T (t - T), R_T (t - T) s_T / s_t)

$$

- where

-$a_T (t - T)$ and $R_T (t - T)$

with

$$

a_T (t - T) = m_T - B_T [a_{T+1} - a_T (t - T + 1)]

$$

$$

R_T (t - T) = C_T - B_T [R_{T+1} - R_T (t - T + 1)] B^\top_T

$$

with

$$

B_T = C_T G^\top_{T+1} R^{-1}_{T+1}, \quad a_T (0) = m_T , \quad R_T (0) = C_T.

$$

::: {.callout-note collapse="true"}

## Video Transcript {.unnumbered}

{{< include transcripts/c4/04_week-4-normal-dynamic-linear-models-part-ii/02_bayesian-inference-in-the-ndlm-part-ii/01_filtering-smoothing-and-forecasting-unknown-observational-variance.en.txt >}}

:::

## Summary of Filtering, Smoothing and Forecasting Distributions, NDLM unknown observational variance :spiral_notepad:

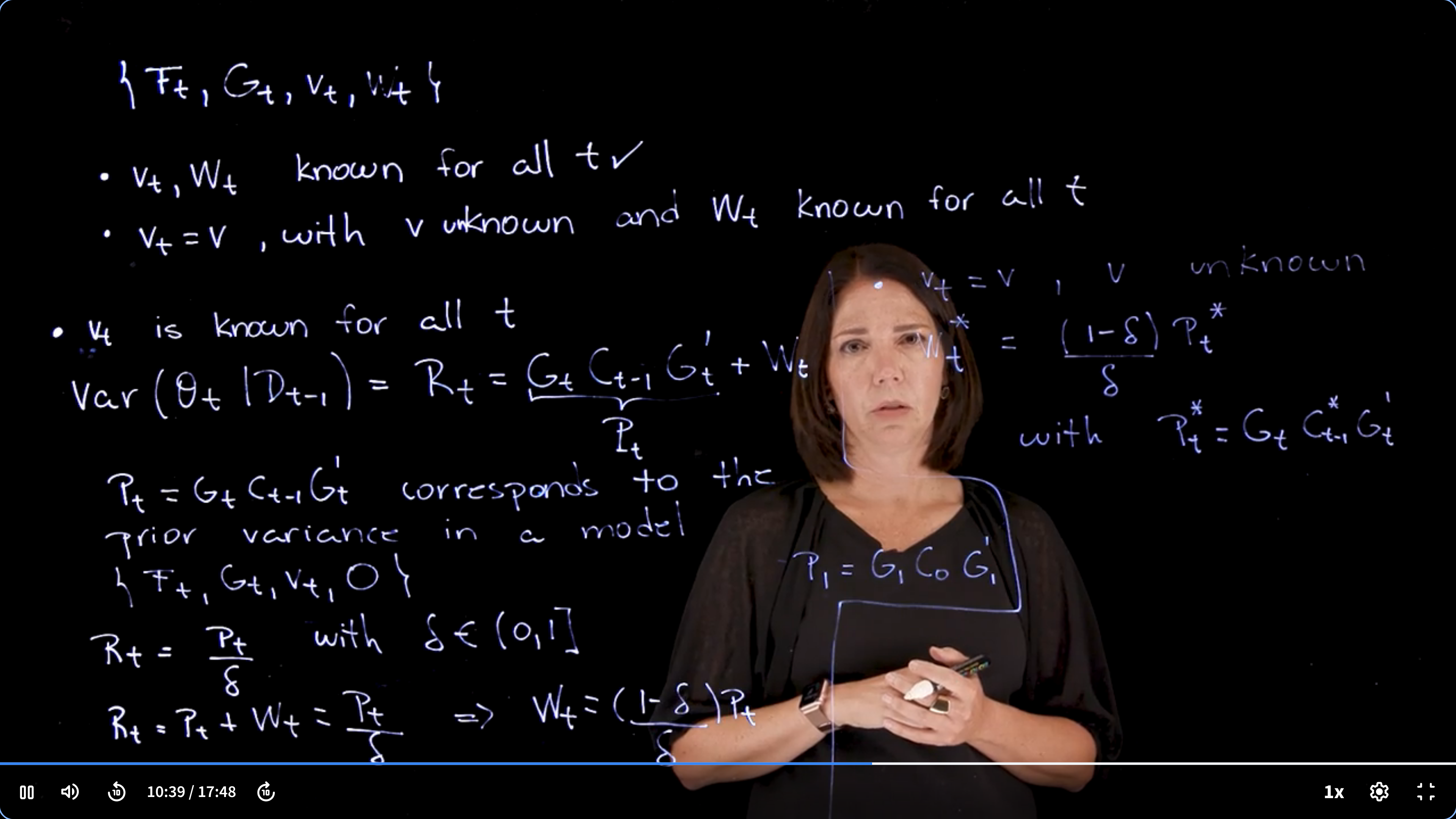

## Specifying the system covariance matrix via discount factors :movie_camera:

{#fig-specifying-the-system-covariance-matrix-via-discount-factors .column-margin group="slides" width="53mm"}

{#fig-specifying-the-system-covariance-matrix-via-discount-factors .column-margin group="slides" width="53mm"}

### Recap and overview

- So far we discussed $\{F_t,G_t,v_t,w_T\}$ with:

- $\underbrace{v_t}_{known}, \underbrace{w_t}_{known}$

- $v_t=\underbrace{v}_{unknown},\qquad \underbrace{w_t}_{known} \forall t$

- We move on to the case where:

- $v_t=\underbrace{v}_{known}, \forall t$ i.e. known observational variance

### Known observational variance with a discount factor \delta

$$

var(\theta_t\mid\mathcal{D}_t)=R_t=\underbrace{G_t C_{t-1}}_{P_t} G^\top_t + W_t

$$

- where $P_t = G_t C_{t-1}$ corresponds to the prior variance in the model with zero system variance i.e. $\{F_t,G_t,v_t,0\}$ with constant parameters that do not evolve over time!

- $R_t=\frac{P_t}{\delta} \qquad \delta \in (0,1]$

- $R_t P_t + W_t = \frac{P_t}{\delta} \implies W_t = \frac{1-\delta}{\delta}P_t$

we estimate

$$

P_1=G_1C_0G_1^T

$$

### Unknown constant observational variance with a discount factor \delta

$$

W_t^{*} = \frac{1-\delta}{\delta} P_t^{*}

$$

where:

$P_T^*=G_1C_0^*G_1^T$

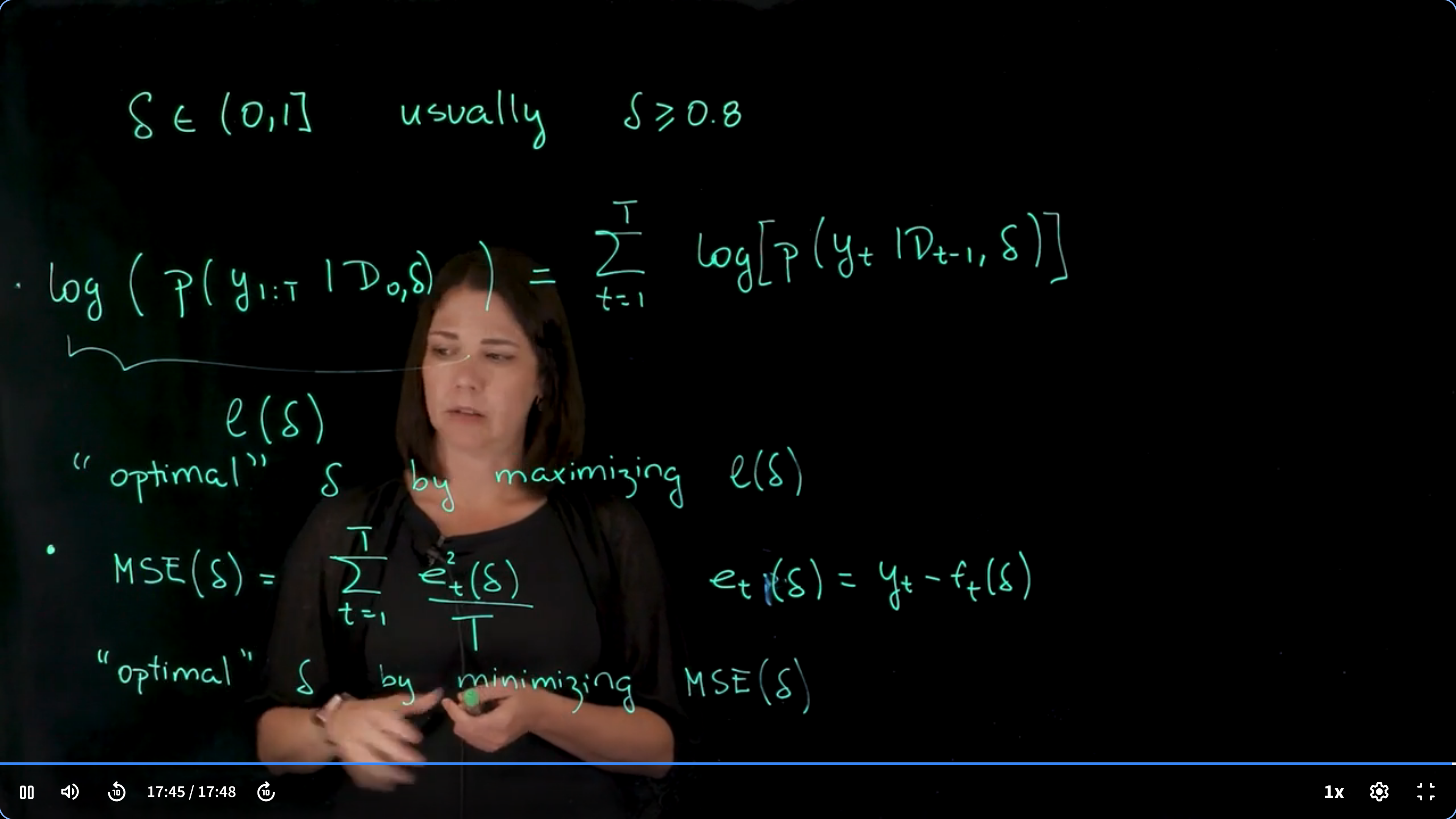

### Estimating $\delta$

$\delta\in(0,1] \text{ usually }\geq 0.8$

$$

\underbrace{\log(p(y_{1:T})\mid \mathcal{D}_0,\delta))}_{l(\delta)} = \sum log(p(y_t\mid \mathcal{D}_{t-1},\delta))

$$

we pick the optimal delta by maximizing $\mathcal{l}(\delta)$

$$

\textrm{MSE}(\delta) = \arg\max_{\delta} \mathcal{l}(\delta)) = \frac{1}{T}\sum_{t=1}^T (y_t - f_t(\delta))^2

$$

optimal $\delta$ is found by minimizing $MSE(\delta)$

but there are a number of methods to estimate $\delta$

we can have one delta for each component.

we can include it in the model and estimate it from the data.

::: {.callout-note collapse="true"}

## Video Transcript {.unnumbered}

{{< include transcripts/c4/04_week-4-normal-dynamic-linear-models-part-ii/02_bayesian-inference-in-the-ndlm-part-ii/03_specifying-the-system-covariance-matrix-via-discount-factors.en.txt >}}

:::

## NDLM, Unknown Observational Variance: Example :movie_camera:

This is a walk though of the R code in @lst-NDLM-unknown-variance

::: {.callout-note collapse="true"}

## Video Transcript {.unnumbered}

{{< include transcripts/c4/04_week-4-normal-dynamic-linear-models-part-ii/02_bayesian-inference-in-the-ndlm-part-ii/04_ndlm-unknown-observational-variance-example.en.txt >}}

:::

## code: NDLM, Unknown Observational Variance Example :spiral_notepad: $\mathcal{R}$

This code allows time-varying $F_t$, $G_t$ and $W_t$ matrices and assumes an unknown but constant $\nu$.

It also allows the user to specify $W_t$ using a discount factor $\delta \in (0,1]$ or assume $W_t$ known.

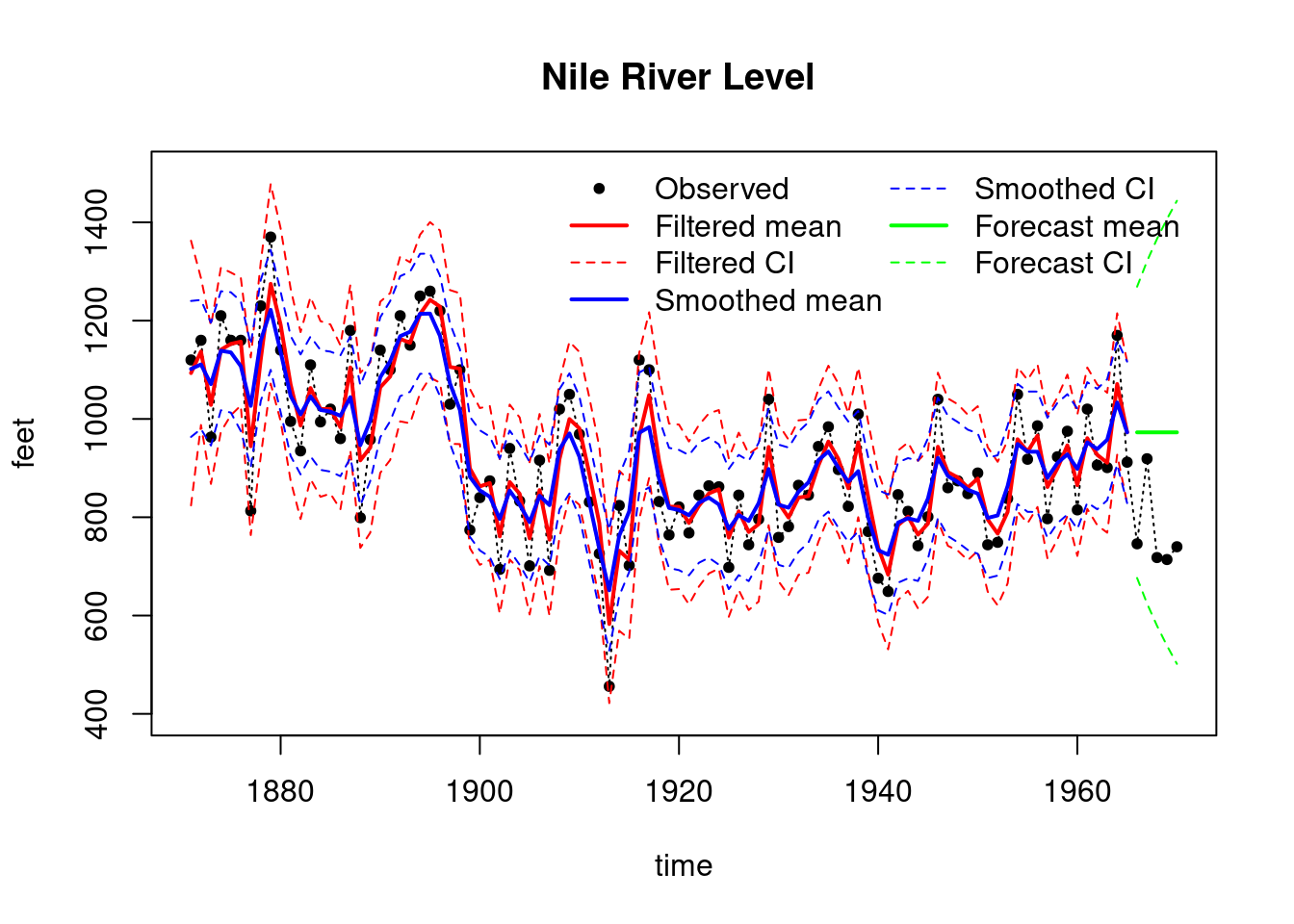

### Nile River Level Filtering Smoothing and Forecasting Example

```{r}

source('all_dlm_functions_unknown_v.R')

source('discountfactor_selection_functions.R')

## Example: Nile River Level (in 10^8 m^3), 1871-1970

## Model: First order polynomial DLM

plot(Nile)

n=length(Nile) #n=100 observations

k=5

T=n-k

data_T=Nile[1:T]

test_data=Nile[(T+1):n]

data=list(yt = data_T)

## set up matrices for first order polynomial model

Ft=array(1, dim = c(1, 1, n))

Gt=array(1, dim = c(1, 1, n))

Wt_star=array(1, dim = c(1, 1, n))

m0=as.matrix(800)

C0_star=as.matrix(10)

n0=1

S0=10

## wrap up all matrices and initial values

matrices = set_up_dlm_matrices_unknown_v(Ft, Gt, Wt_star)

initial_states = set_up_initial_states_unknown_v(m0,

C0_star, n0, S0)

## filtering

results_filtered = forward_filter_unknown_v(data, matrices,

initial_states)

ci_filtered=get_credible_interval_unknown_v(results_filtered$mt,

results_filtered$Ct,

results_filtered$nt)

## smoothing

results_smoothed=backward_smoothing_unknown_v(data, matrices,

results_filtered)

ci_smoothed=get_credible_interval_unknown_v(results_smoothed$mnt,

results_smoothed$Cnt,

results_filtered$nt[T])

## one-step ahead forecasting

results_forecast=forecast_function_unknown_v(results_filtered,

k, matrices)

ci_forecast=get_credible_interval_unknown_v(results_forecast$ft,

results_forecast$Qt,

results_filtered$nt[T])

```

```{r}

#| label: fig-NDLM-unknown-variance-nile-data

#| fig-cap: Nile River Level Filtering, Smoothing and Forecasting Results

## plot results

index=seq(1871, 1970, length.out = length(Nile))

index_filt=index[1:T]

index_forecast=index[(T+1):(T+k)]

plot(index, Nile, main = "Nile River Level ",type='l',

xlab="time",ylab="feet",lty=3,ylim=c(400,1500))

points(index,Nile,pch=20)

lines(index_filt,results_filtered$mt, type='l', col='red',lwd=2)

lines(index_filt,ci_filtered[, 1], type='l', col='red', lty=2)

lines(index_filt,ci_filtered[, 2], type='l', col='red', lty=2)

lines(index_filt,results_smoothed$mnt, type='l', col='blue',lwd=2)

lines(index_filt, ci_smoothed[, 1], type='l', col='blue', lty=2)

lines(index_filt, ci_smoothed[, 2], type='l', col='blue', lty=2)

lines(index_forecast, results_forecast$ft, type='l',

col='green',lwd=2)

lines(index_forecast, ci_forecast[, 1], type='l',

col='green', lty=2)

lines(index_forecast, ci_forecast[, 2], type='l',

col='green', lty=2)

legend("topright",

legend = c("Observed", "Filtered mean", "Filtered CI",

"Smoothed mean", "Smoothed CI",

"Forecast mean", "Forecast CI"),

col = c("black", "red", "red", "blue", "blue", "green", "green"),

lty = c(NA, 1, 2, 1, 2, 1, 2),

pch = c(20, NA, NA, NA, NA, NA, NA),

lwd = c(NA, 2, 1, 2, 1, 2, 1),

bty = "n",

ncol = 2)

```

::: {.callout-note collapse="false"}

## Overthinking the Nile River Data {.unnumbered}

We use the Nile dataset throughout the course, despite the Nile data being notorious for having long term dependencies and being highly non-linear, which might present many challenges for the NDLM framework. c.f. the joint work of two giants [Benoit Mandelbrot](https://en.wikipedia.org/wiki/Benoit_Mandelbrot) and [Harold Edwin Hurst](https://en.wikipedia.org/wiki/Harold_Edwin_Hurst).

Which led to the development of the Hurst exponent and the [fractional Brownian motion](https://en.wikipedia.org/wiki/Fractional_Brownian_motion), i.e. fractional Gaussian noise and fractional ARIMA [ARFIMA](https://en.wikipedia.org/wiki/Autoregressive_fractionally_integrated_moving_average) which are more suitable for modeling the Nile data but not covered in this course.

Just a couple of concepts here:

In Fractional Brownian Motion (fBm) draws from the Normal need not be independent. With the concept of Hurst exponent $H$ which is a measure of the long-term memory of a time series. The Hurst exponent is defined as follows:

$$

\mathbb{E}[B_{H}(t)B_{H}(s)]={\tfrac {1}{2}}(|t|^{2H}+|s|^{2H}-|t-s|^{2H}),

$$ {#eq-fbm-autocovariance}

- where:

- $B_{H}(t)$ is the fractional Brownian motion, and

- $H$ is the Hurst exponent.

2. in ARFIMA, the autocovariance we allow the exponent of the lag $k$ to be a real number $d$ rather than an integer, i.e. we allow for fractional differencing via a formal binomial series expansion of the form:

$$\begin{array}{c} {\displaystyle {\begin{aligned}(1-B)^{d}&=\sum _{k=0}^{\infty }\;{d \choose k}\;(-B)^{k}\\&=\sum _{k=0}^{\infty }\;{\frac {\prod _{a=0}^{k-1}(d-a)\ (-B)^{k}}{k!}}\\&=1-dB+{\frac {d(d-1)}{2!}}B^{2}-\cdots \,.\end{aligned}}} \end{array}

$$ {#eq-ARFIMA}

:::

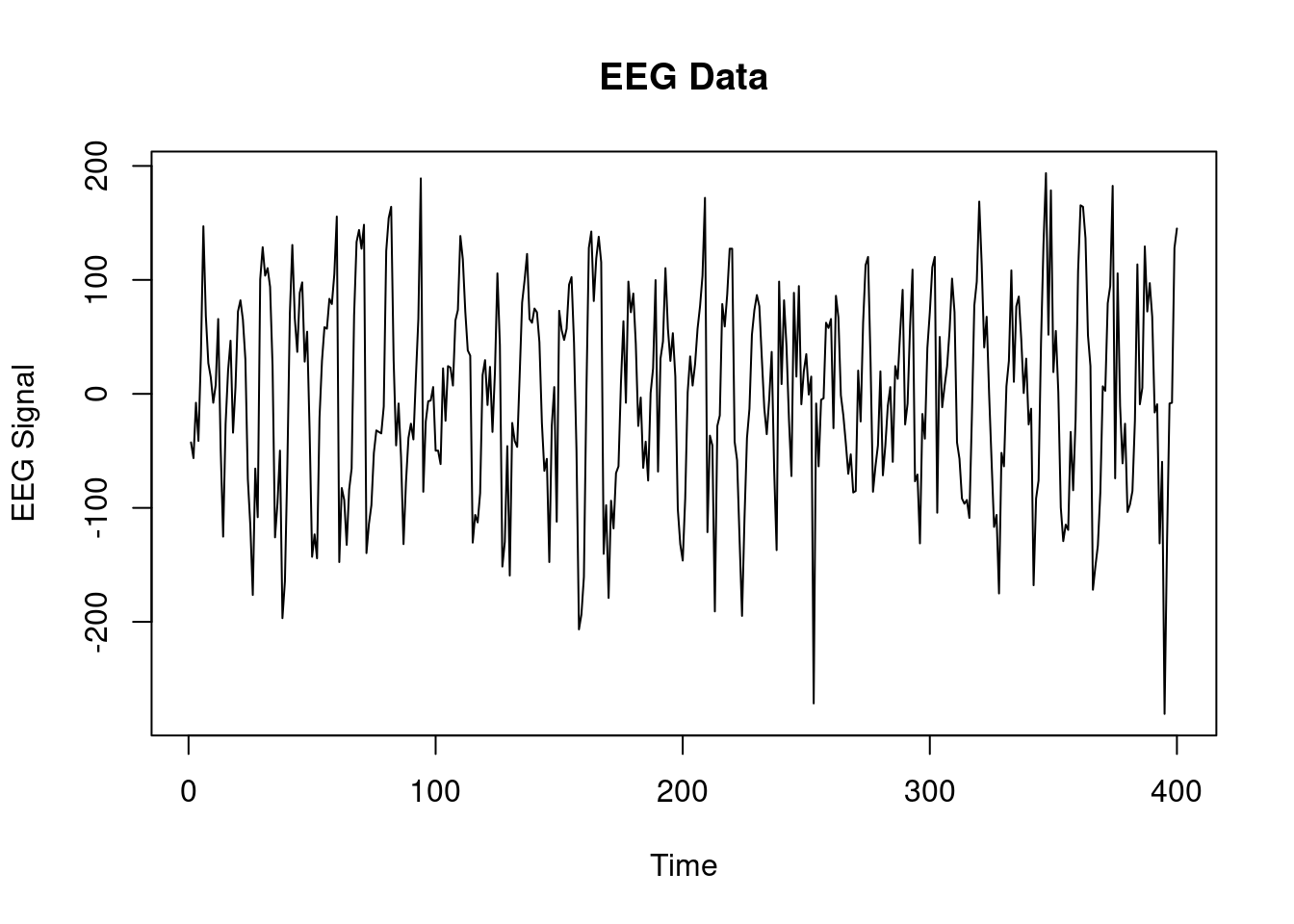

## Case Study EEG data :movie_camera: {#section-NDLM-eeg}

```{r}

### EEG example ##################

source('all_dlm_functions_unknown_v.R')

source('discountfactor_selection_functions.R')

eeg_data <- scan("data/eeg.txt")

length(eeg_data)

eeg_data_gh <- scan("data/eeg_gh.txt")

length(eeg_data_gh)

plot(eeg_data, type='l', main="EEG Data", xlab="Time", ylab="EEG Signal")

head(eeg_data)

head(eeg_data_gh)

T <- length(eeg_data)

data <- list(yt = eeg_data[])

```

::: {.callout-note collapse="true"}

## Video Transcript

{{< include transcripts/c4/04_week-4-normal-dynamic-linear-models-part-ii/03_case-studies/01_eeg-data.en.txt >}}

:::

## Case Study: Google Trends :movie_camera: {#section-NDLM-google-trends}

```{r}

```

::: {.callout-note collapse="true"}

## Video Transcript

{{< include transcripts/c4/04_week-4-normal-dynamic-linear-models-part-ii/03_case-studies/02_google-trends.en.txt >}}

:::